Same Voltage, Two Outcomes: Why AI in Electrical Distribution is Won on Change, Not Technology

July 15, 2026

By Jerome Potvin · Director of Commercial Strategy · Innovair Group

Every distributor plugs in the same technology. What sets them apart isn’t the algorithm — it’s their ability to bring their people along. And the correlation is relentless.

In electrical distribution, we know one thing better than anyone: a conductor, however high-performance, is useless until the circuit is closed. Artificial intelligence obeys exactly the same law. The technology is ready, the data exists, vendors are knocking at the door — but the circuit only closes the moment field teams adopt it. And that is precisely where everything is decided: in change management.

Canada’s electrical products distribution market closed 2025 at $17.6 billion in sales, up 3.9%, according to the benchmark Pathfinder study. Ontario accounts for 36.5% of national volume, followed by Quebec and Alberta. Behind these figures lies a structural reality: more than 82% of the market is now in the hands of multinational distributors, spread across 1,536 branches and nearly 22,000 employees nationwide.1

Concretely, this market has a face. In Quebec, names like Guillevin — an electrical distributor founded in Montreal in 1906, today some 140 points of sale, with a transactional website and a Greentech division dedicated to sustainable products — or Lumen, Sonepar’s Quebec banner. Elsewhere in the country, Westburne and Nedco (Rexel), EECOL (Wesco) or Texcan (Sonepar) blanket the territory. Most of these names, once independent, have become banners of global giants — which explains the market’s concentration.4

01 / THE MARKET

A sector under tension

The backdrop has never been more favourable. The electrification of Canada’s economy is driving unprecedented demand: national forecasts project electricity demand rising 62 to 112% by 2050, which will require roughly doubling supply. Cumulative investment in transmission and distribution networks could approach $700 billion by 2050.2 In April 2026, Ottawa formalized this trajectory with its national strategy Powering Canada Strong, placing grid modernization, data centres and EV charging infrastructure at the heart of economic growth.3

For the distributor, this means more volume, but also more complexity: longer project cycles, pressure on raw materials like copper, and customers — contractors, integrators, data-centre operators — who demand a buying experience as smooth as B2C. It is precisely this complexity that AI promises to absorb.

And Quebec — the country’s second-largest distribution market — embodies this transition better than any other province. With its 2035 Action Plan, Hydro-Québec projects demand rising 60 TWh by 2035 and a doubling of consumption by 2050, backed by $155 to 185 billion in investment — three to four times the annual average of the past five years.5 The plan explicitly aims to transform how buildings are heated, in a province where electricity already provides most residential heating. Hydro-Québec is even distributing smart thermostats free of charge: a clear signal that the future of heating will be both electric and data-driven.

$155–185B

investments planned by Hydro-Québec through 2035 — 3 to 4 times the recent annual average5

02 / HVAC

The same wave hits heating and cooling

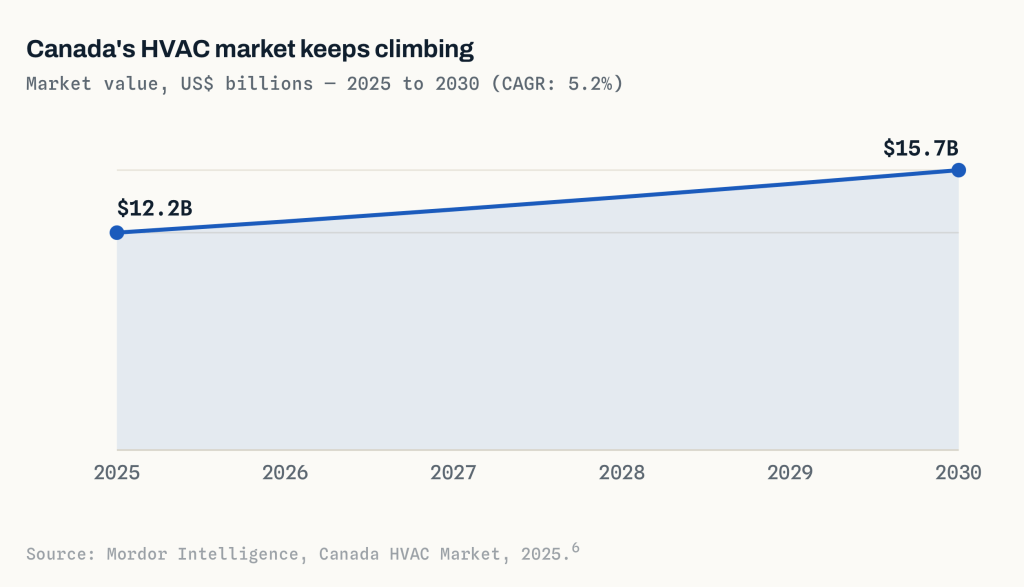

You cannot discuss electrical distribution in Canada without discussing HVAC. Heating, ventilation and air conditioning are the natural extension of electrification: as the country moves away from fossil fuels, heat itself becomes an electric product. Canada’s HVAC market is estimated at US$12.2 billion in 2025 and is expected to reach $15.7 billion by 2030, a 5.2% annual growth rate.6 Heating alone absorbs nearly two-thirds of the country’s residential energy — a playground directly adjacent to our aisles.

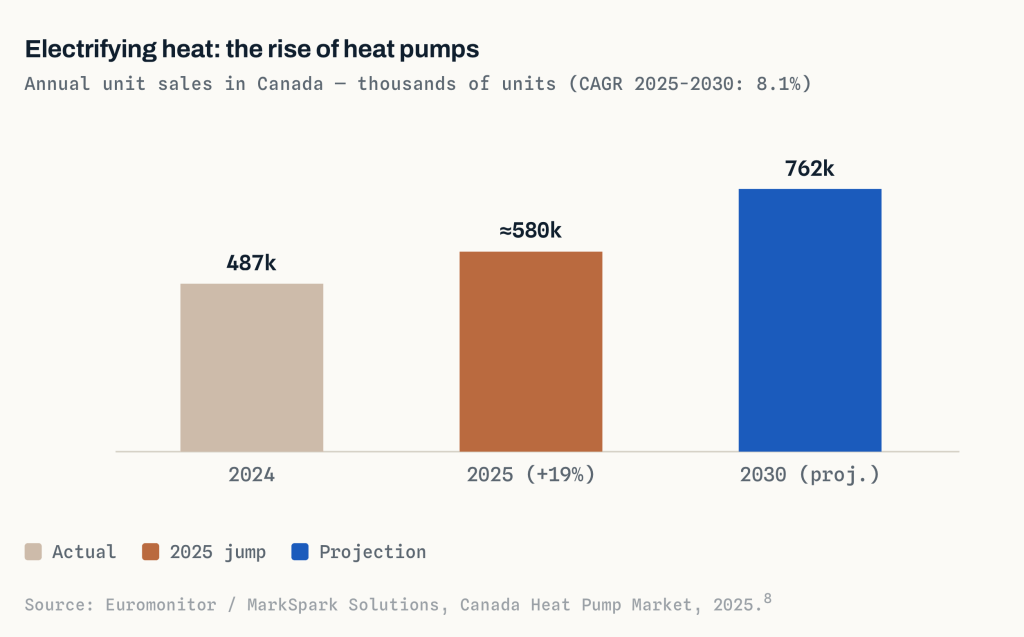

The engine of this growth has a name: the heat pump. Boosted by carbon pricing and a stack of federal and provincial subsidies, heat-pump sales in Canada jumped 19% in 2025. The Oil to Heat Pump Affordability Program alone had funded 274,000 residential installations as of November 2025, 68% of them cold-climate units (−25 °C).7 In Quebec, the Chauffez vert program brought the homeowner’s net cost down to about $3,500, propelling regional installations up 34% in a year.7

For the distributor, this shift redraws inventory: inverter compressors, cold-climate heat pumps, baseboards and hybrid systems now sit alongside traditional electrical products. And AI is already moving in: smart controls that dynamically tune the heat pump to weather and grid demand, predictive maintenance, energy optimization.9 But HVAC also shares the sector’s Achilles’ heel: an acute shortage of qualified technicians is already slowing timelines in Ontario, British Columbia and Quebec.

Quebec’s HVAC industry, for that matter, isn’t watching AI from afar. The Master Group — Canada’s largest independent HVAC-R distributor, based in Boucherville, with 68 branches — turned its 2026 MPower Summit in Montreal into a showcase where “AI in distribution” shared the bill with decarbonization… and managing stress and change.10 Wolseley Canada, a national plumbing and HVAC distributor with more than 200 branches, is betting on Wolseley Express, which it bills as the industry’s most robust e-commerce platform.11

03 / RETAIL AND DIGITAL

The customer is already buying online

While we debate AI, our customers have already changed. Business-to-business (B2B) e-commerce in North America is worth US$6.14 trillion in 2026 and is growing nearly 19% a year.12 Better still: 87% of B2B buyers say they will pay more for a supplier with an excellent online portal, and 94% feel a unified (omnichannel) buying experience makes them more productive.12 The average B2B company now derives 82% of its revenue from remote interactions, and Amazon Business alone generated some US$83 billion in 2025.13

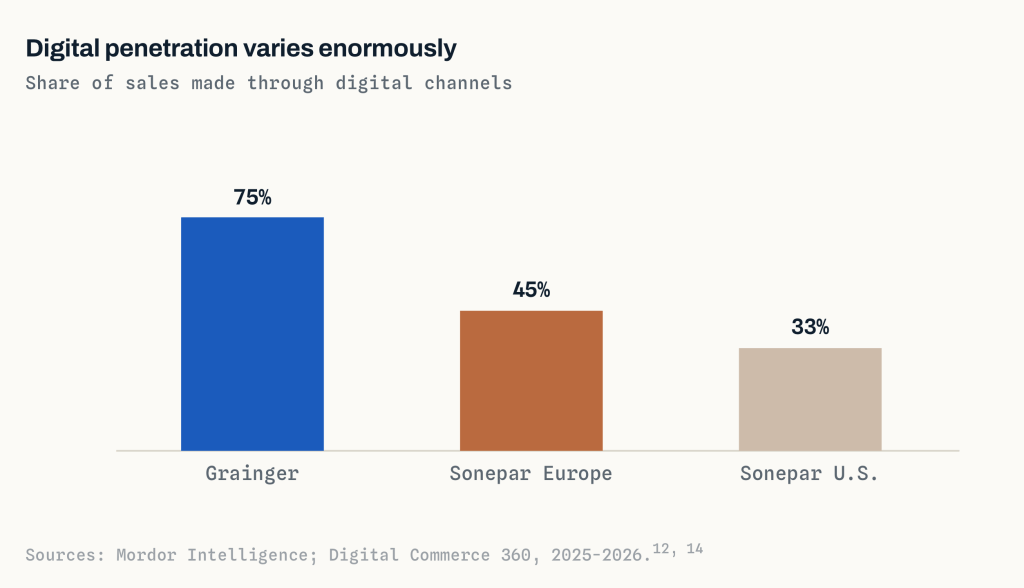

Electrical and HVAC distribution is no exception. The giant Grainger already makes 75% of its sales digitally; Sonepar, as noted, reaches 45% in Europe and 33% in the United States; at home, Guillevin and Wolseley Express are building transactional platforms tailored to tradespeople.14 The maturity gap is enormous — and it already separates the winners from the rest.

The trap would be to pit the click against the counter. The best distributors instead see a blended journey: the customer starts online, consults a rep, then picks up at the branch — physical and digital interweave within a single transaction. And maturity pays: according to Deloitte, the most digitally mature B2B suppliers beat their sales targets by a 110% greater margin than the least mature.15 Yet reaching that maturity isn’t an IT project: it’s a change project.

04 / THE TECHNOLOGY

AI is no longer a hypothesis

Adoption has tipped. In the United States, about 18% of firms were using AI in late 2025, and more than 20% planned to in the first half of 2026; generative-AI use already reaches nearly 41% of the workforce.16 In B2B sales, organizations deploying AI post revenue growth of 13 to 15% and a 10 to 20% improvement in commercial performance.17

The sector is deploying. Sonepar, the world’s leading electrical distributor, posted record sales of $37.9 billion in 2025, including $13.9 billion online — a 50% jump in one year via its omnichannel platform Spark.14 In 2026, the company is rolling out worldwide, with Microsoft, an agentic AI it describes as an “exoskeleton” for its 24,000 sales advisors.18 At Rexel, present in 26 countries, a demand-forecasting model combines weather data, permit calendars and seasonality to pre-position stock 6 to 8 weeks ahead; in France and Germany, contractors finding product available at peak shifted a share of their purchases on their own — without any rep ever having to ask.19

The technology works. The real variable is whether your people know how — and want — to use it.

05 / THE BOTTLENECK

Change, the conductor we forget

Here is the statistic every executive should pin to the wall: 70% of major transformations fail, and employee resistance accounts for up to 72% of those failures.20 In other words, AI almost never fails for technical reasons — it fails because change is neglected. The knowledge has existed for twenty years; it’s the execution that’s missing.

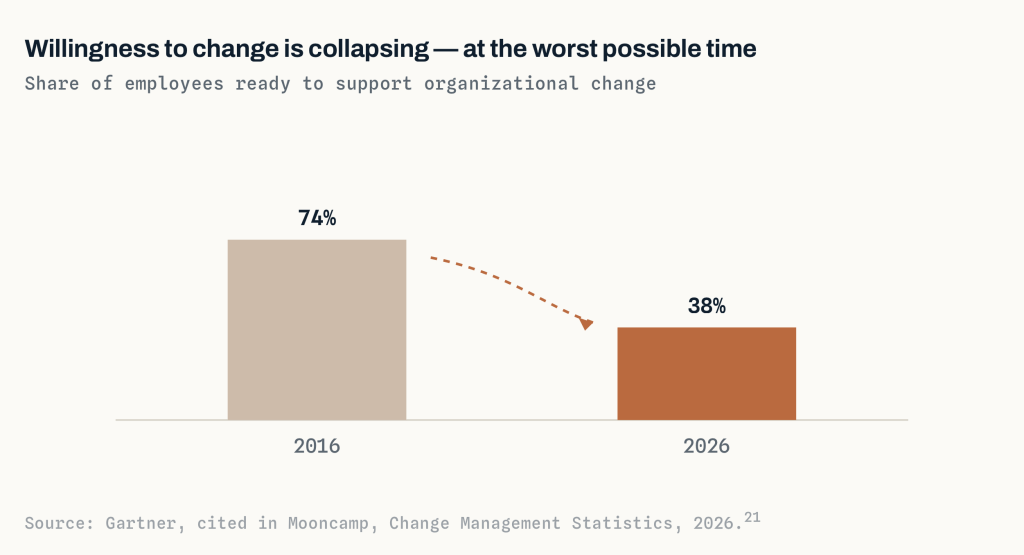

And the ground has hardened. Only 38% of employees say they’re ready to support organizational change today, versus 74% in 2016 — a halving in less than a decade.21 Change fatigue is real, and each new technology wave makes it worse.

In electrical distribution, this resistance has a precise face. It’s the seasoned rep who has managed 80 accounts on instinct for 25 years and is suddenly asked to trust a “next best action” generated by an algorithm. It’s the counter clerk who sees automation and hears “replacement.” Change isn’t a module you bolt on at the end of an AI project: it’s the main conductor, the one without which no current flows.

06 / THE CORRELATION

What the data proves

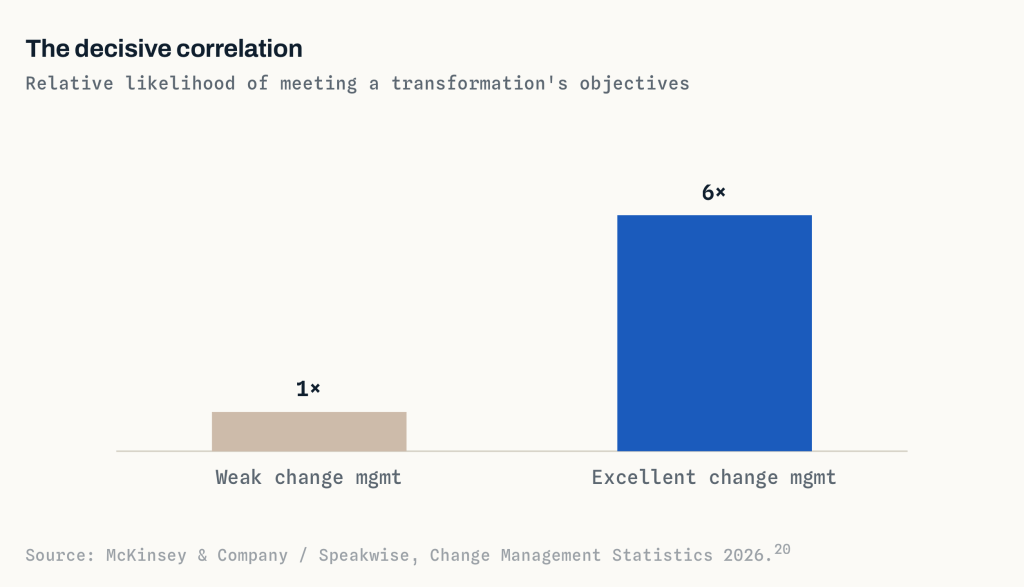

If resistance causes failure, the reverse is just as true — and measurable. The correlation between the quality of change management and a transformation’s success is one of the most robust in the management literature. Projects with excellent change management are six times more likely to meet their objectives, with returns reaching as high as 143%.20

This correlation has a direct consequence for anyone deploying AI: the decisive variable isn’t the model, it’s the adoption method. And AI can itself serve change management — organizations that apply it there report up to 30% fewer project delays and 25% higher productivity.22 The loop closes: you use AI to better drive the adoption of AI.

6×

more success for projects with excellent change management20

07 / THE OPERATING ROOM

Roles played to the letter

An operating room doesn’t succeed because of the best scalpel. It succeeds because every role is defined and executed to the letter: the surgeon leads, the anesthesiologist watches the vital signs, the nurses manage the surgical field, the scrub tech hands over the right instrument at the right second. No one improvises; a checklist frames every move; responsibilities are crystal clear. An AI-driven transformation is exactly that theatre — and the leading cause of failure is blurred roles.

The executive sponsor is the lead surgeon. Since 1998, in every one of Prosci’s benchmark studies, active and visible sponsorship by a leader has been the number-one success factor — cited three times more often than the next. The figures are unequivocal: a project with a highly effective sponsor meets its objectives 79% of the time, versus 27% with an ineffective one. Yet nearly half of executives don’t understand their role as sponsor.23

Around the sponsor, every role counts. The change manager plays the anesthesiologist: neutral and dedicated, monitoring the vital signs of adoption and holding the course — and a dedicated change resource multiplies the odds of success sixfold. Branch managers and front-line managers are the nurses at the team’s bedside: they translate, reassure, accompany — all the more so since managers alone account for 70% of the variance in engagement, while often being the most resistant group. Field champions, finally, are the scrub tech: operational credibility, the right move at the right moment. And the surgical checklist has its equivalent: a clear responsibility matrix — who decides, who executes, who is consulted, who is informed.23

In an operating room, no one improvises. A transformation that succeeds doesn’t either: everyone plays their role to the letter.

08 / THE EUROPEAN MIRROR

What Europe teaches us

To guess the next 18 Canadian months, it’s often enough to look at Europe — a more digitally mature market, and a mirror of what awaits us. Concrete examples abound. Rexel — €19.4 billion in sales in 2025, nearly half of it in Europe — appointed a chief digital officer to its executive committee in 2025 and is rolling out its Energeasy Solarplatform (self-consumption management, EV charging, heat pumps) under its Rexel France and Elektroskandia banners in the Nordics.24 On the HVAC side, Rexel absorbed the Dutch firm Wasco — 35 branches — for €485 million, betting on the Netherlands’ heating market.25 Sonepar, for its part, is building a genuine HVAC vertical in France through acquisitions (Hydeclim, CD Sud), a segment that already topped €320 million as early as 2022.26

The context there is also more pressing. The European Union and Norway will need to invest an average of €67 billion a year through 2050 to modernize their distribution networks, while only about €33 billion is spent today.27 In December 2025, Brussels unveiled its European Grids Package to speed up connections and permits.28 Europe’s smart-grid market is growing nearly 16% a year and could quadruple by 2034;29 low-voltage distribution there is rising 4.5 to 6% a year, driven by REPowerEU.30

But Europe also offers a warning. Despite its digital lead, the margins of the four global distribution giants — Sonepar, Rexel, Graybar, Wesco — have compressed, falling from around 7% in 2022 to 5.5% in 2024.31 The lesson is clear: technology and volume aren’t enough to protect profitability. What sets you apart for the long run is the ability to transform the organization — so, once again, change.

Europe doesn’t prove that AI is enough. It proves the lead goes to those who know how to manage change.

09 / LESSONS LEARNED

What to take away

The next 12 to 18 months will see the shift from assistant to agent: a February 2026 Deloitte study reveals that while 45% of B2B suppliers use AI in sales, only 24% have touched agentic AI — the kind that actually executes workflows.15 The gap will widen fast, in a two-speed market. Here, in summary, is what the data and the field teach us.

1. Technology is the easy part.

AI almost never fails for technical reasons. It fails when change is neglected. That’s the thread running through everything above.

2. The correlation is proven, not intuitive.

Excellent change management means six times more success. Treat it as a measurable investment, with its own adoption metrics.

3. Define roles to the letter.

As in an operating room, it all starts with an active, visible sponsor, surrounded by a dedicated change manager, equipped front-line managers and credible champions. Blurred roles kill more projects than technology does.

4. Digital is no longer optional.

When 87% of B2B buyers pay more for an excellent portal, starting where friction is low — demand forecasting, project quoting, product recommendation — proves value before scaling.

5. Augment, don’t replace — and stay clear-eyed.

Human plus AI always beats AI alone or human alone. But beware the hype: Gartner predicts more than 40% of agentic-AI projects will be abandoned by 2027, for lack of demonstrated value or controlled costs.32 The pilot that never reaches production is the most common trap.

Same voltage, two outcomes: it won’t be the distributor with the best model who wins, but the one who best managed the change.

In our trade, you learn early that an open circuit carries no energy, however elegant the wiring. AI changes the game for Canadian electrical distribution — on one condition. The current doesn’t flow on its own.

Sources

- Channel Marketing Group / Electrical Trends, “The Size of the Canadian Electrical Market” (Pathfinder Benchmark, vol. 41), 2025. electricaltrends.com

- Electro-Federation Canada, Grid Technology Roadmap — Final Report, April 2026. electrofed.com

- Natural Resources Canada, Powering Canada Strong, 2026. natural-resources.canada.ca

- Canadian Electrical Wholesaler, Guillevin International profile, 2025. canadianelectricalwholesaler.ca

- Hydro-Québec, 2035 Action Plan, 2023-2024. hydroquebec.com

- Mordor Intelligence, Canada HVAC Market, 2025. mordorintelligence.com

- Mordor Intelligence, Canada HVAC Equipment Market (oil-to-heat-pump conversion; Chauffez vert), January 2026. mordorintelligence.com

- Euromonitor International / MarkSpark Solutions, Canada Heat Pump Market, 2025. marksparksolutions.com

- Insights Leader, Canada Heat Pump Market — Technology & Innovation Impact, 2025. insightsleader.com

- Master Group, MPower Summit 2026 (program: AI in distribution, decarbonization, stress management), February 2026. master.ca

- Wolseley Canada, Wolseley Express e-commerce platform, 2026. wolseleyinc.ca

- Mordor Intelligence, North America B2B E-commerce Market (US$6.14T; 87% pay more; Grainger 75%), January 2026. mordorintelligence.com

- Capital One Shopping Research, B2B eCommerce Statistics (Amazon Business; 82% of revenue remote), 2026. capitaloneshopping.com

- Digital Commerce 360, “Sonepar digital sales jump 50% to $13.9 billion in 2025” (digital: 33% U.S., 45% Europe), March 2026. digitalcommerce360.com

- Deloitte Digital, B2B study on AI and digital maturity (+110% margin; agentic AI 24%), February 2026. via uncap.com

- U.S. Federal Reserve, Monitoring AI Adoption in the U.S. Economy, April 2026. federalreserve.gov

- McKinsey, cited in MarketBetter, “AI in B2B Sales: What’s Actually Working in 2026,” March 2026. marketbetter.ai

- Electrical Trends, “Sonepar and AI,” February 2026. electricaltrends.com

- Canadian Electrical Wholesaler, “How AI is Reshaping Channel Sales and Distributor Relationships,” 2026. canadianelectricalwholesaler.ca

- McKinsey & Company / Speakwise, Change Management Statistics 2026. speakwiseapp.com

- Gartner (2022), cited in Mooncamp, Change Management Statistics, 2026. mooncamp.com

- PwC, cited in AMS Consulting, “AI and Change Management,” 2025. amsconsulting.com

- Prosci, Best Practices in Change Management / roles and sponsorship (effective sponsor 79% vs 27%; dedicated resource 6×), 2026. prosci.com

- Rexel, Energeasy Solar platform and digital strategy (Rexel France, Elektroskandia), 2026. ad-hoc-news.de

- HVACR Trends, “Rexel buys HVACR distributor in Europe” (Wasco acquisition, Netherlands, €485M), 2023. hvacrtrends.com

- Sonepar, “Sonepar Reinforces its HVAC Expertise with the Acquisition of Hydeclim” (France HVAC vertical > €320M). sonepar.com

- Eurelectric, Grids for Speed (€67B/yr grid investment through 2050), 2024. eurelectric.org

- European Commission, European Grids Package (COM/2025/1005), December 2025. energy.ec.europa.eu

- Market Data Forecast, Europe Smart Grid Market (CAGR 15.67%), 2026. marketdataforecast.com

- IndexBox, European Union 380V/400V Power Distribution Market (4.5–6%), 2026. indexbox.io

- EthiFinance, Sonepar SAS rating (sector EBIT margins 7.0% in 2022 to 5.5% in 2024), 2025. ethifinance.com

- Gartner, agentic-AI forecast, cited in MarketBetter, 2026. marketbetter.ai

Data accessed June 2026. Market statistics reflect the reference periods indicated by each source.