Hammond Power Solution’s Breakout Year: Canadian Transformer Maker Leads Electrical Stock Market

July 13, 2026

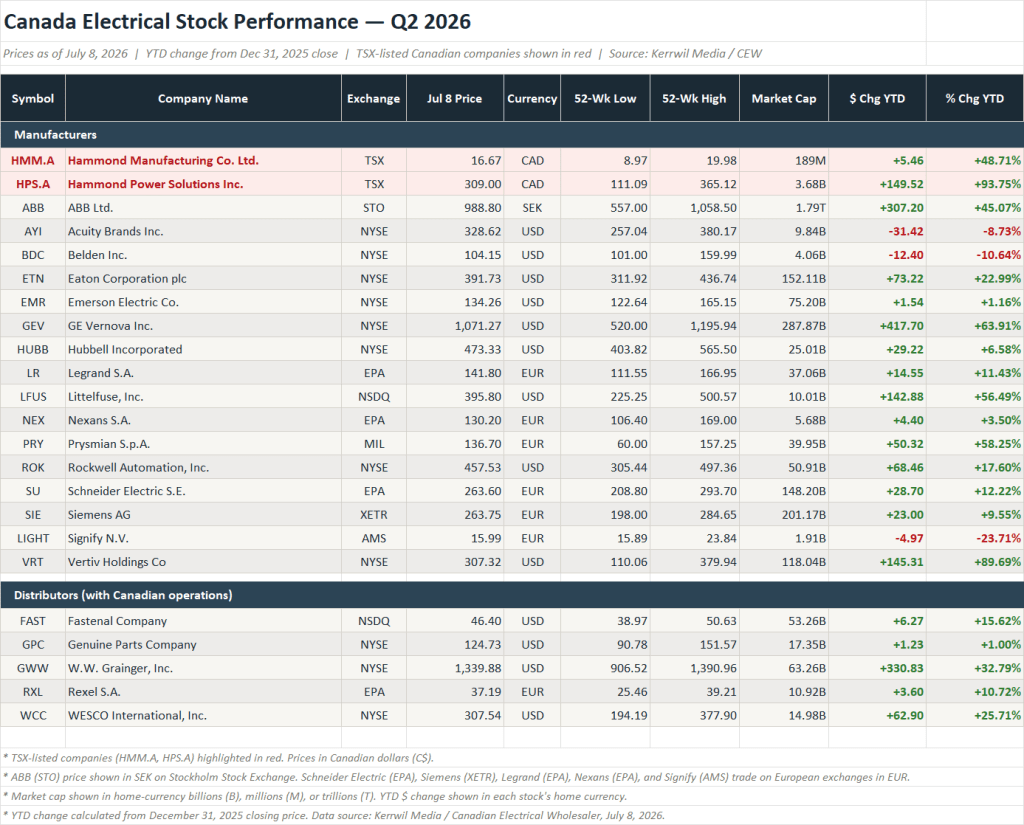

Q2 2026 electrical stock data shows the infrastructure buildout is no longer a thesis it’s showing up in market capitalization, with two Canadian manufacturers posting the strongest gains in the entire peer group.

Electrical equipment and distribution stocks tracked by Canadian Electrical Wholesaler turned in a broadly positive first half of 2026, with the majority of manufacturers and all five tracked distributors posting gains through July 8. The data, compiled by CEW using real-time market pricing, points to a sector being re-rated on the back of data centre construction, grid modernization spending, and a wave of reshored industrial capital investment across North America. For a channel that spent much of the past two years navigating supply normalization and price deflation on certain product lines, the equity market’s read on manufacturer fundamentals this quarter is unambiguous: demand visibility into power infrastructure has improved, and investors are paying for it.

The clearest expression of that theme sits at the top of the manufacturers’ table. Vertiv Holdings, whose thermal and power management systems are core infrastructure for hyperscale data centres, gained 89.69% year-to-date, while GE Vernova — spun out to focus squarely on grid and power generation equipment — advanced 63.91%. Littelfuse, a less obvious data-centre name but a direct beneficiary of rising electronic content and power-density requirements, rose 56.49%. ABB also posted a strong 45.07% gain, reinforcing that the electrification and automation buildout is a multinational phenomenon, not a North American curiosity.

Further down the list, Eaton (+22.99%) and Rockwell Automation (+17.60%) confirm that diversified industrial electrical manufacturers are participating in the move as well, even without the pure-play data centre exposure of Vertiv or GE Vernova. The wire and cable segment deserves its own mention. Prysmian, the Milan-listed global cable and wire manufacturer, gained 58.25% year-to-date — one of the strongest performances in the entire manufacturers’ table. Nexans, its French peer, was up a more modest 3.50%, but both names point to the same underlying demand: the sheer volume of cabling required for data centre buildouts, offshore wind interconnection, and grid expansion has re-rated the major cable producers alongside equipment makers.

Not every name benefited, however. Signify finished the period down 23.71% and trading near its 52-week low, underscoring that the pressure facing the commercial and consumer lighting segment has not let up. Acuity Brands (-8.73%) and Belden (-10.64%) also closed the first half in negative territory, a reminder that lighting-heavy portfolios and certain connectivity categories face a different demand environment than power infrastructure.

Distribution names, by contrast, were uniformly positive across the board. WESCO International rose 25.71% and W.W. Grainger climbed 32.79%, with Fastenal up 15.62% — all three among the strongest results in their respective corners of the industrial supply chain. Rexel, the Paris-listed global electrical distributor, gained 10.72%, a solid result for a company with significant Canadian operations. Genuine Parts Company — parent of Motion Industries, one of the largest industrial MRO distributors in North America — posted a more modest +1.00% year-to-date, reflecting the slower pace of the broader industrial MRO segment relative to the electrical infrastructure channel.

For a segment whose stock performance tends to track underlying volume and pricing conditions in the channel more directly than manufacturers do, this breadth of positive results is notable. It suggests that electrical and industrial distribution demand held up well through the second quarter, with no major distributor showing signs of the destocking or margin compression that periodically weighs on the sector.

The Canadian angle in this quarter’s data is impossible to overstate. Hammond Power Solutions, the Guelph-based dry-type transformer manufacturer, posted a 93.75% year-to-date gain — the single best performance of any stock in the table, manufacturer or distributor — with its share price climbing from the low-$100s to $309.00 and its market capitalization reaching $3.68 billion. Its sister company, Hammond Manufacturing, which produces enclosures and electrical components, was not far behind at +48.71%, with shares more than doubling off their 52-week low of $8.97 to close at $16.67.

Both moves reflect the same underlying story: North American investment in transformers, switchgear, and enclosures tied to grid capacity expansion, data centre power delivery, and electrification of industrial infrastructure is flowing directly into the order books — and now the valuations — of Canadian manufacturers positioned in those categories. For a Canadian trade audience, these two TSX-listed names offer the most direct proof point that the infrastructure investment cycle discussed in boardrooms and at industry events is translating into real financial performance domestically, not just among the large U.S. and European suppliers that dominate headlines.

Taken together, the Q2 2026 data reflects something broader than a stock market story. When gains are this widely distributed across transformers, automation, power management, wire and cable, and distribution, in companies headquartered in Canada, the U.S., and Europe — it points to real capital expenditure moving through the channel, not investor enthusiasm running ahead of actual orders. Utilities are building, data centres are under construction, and industrial facilities are being retooled. The companies in this table supply the equipment that makes all of it possible, and their valuations are moving accordingly.

For Canadian wholesalers and distributors, the practical implication is straightforward: the manufacturer partners posting these kinds of numbers are not standing still. Capacity investment, product development, and channel support tend to follow financial performance. The second half of 2026 is worth watching closely.

Data compiled by Canadian Electrical Wholesaler and Kerrwil Media using real-time market data as of July 8, 2026. Year-to-date figures calculated from December 31, 2025 closing prices.

To learn more about Hammond Power Solutions, visit HERE.